DeFi Tokens the Market May Have Mispriced

Executive Summary

DeFi has had a brutal first half. Most tokens are down 40–70% from their cycle highs, and in the sell-off, the market has largely stopped distinguishing between protocols that earn real money and those that don’t.

That gap is the opportunity. A handful of protocols are still generating genuine fees, still routing those fees back to token holders through buybacks, burns, and direct distributions — and still trading as if none of that were happening. When the price falls, but the cash flow holds, the multiple compresses. That is exactly where mispricing lives.

This brief screens our 35-name DeFi universe across three sectors — Perps DEX, DEX/AMM, and Lending — for a rare combination of three traits:

Mature supply. Most of the token is already circulating, so future dilution can’t quietly erode your position.

Live value accrual. The protocol actually returns fees to holders today — not “someday.”

A genuine discount. The token trades cheaper than half its peers on a fee-adjusted (FDV/Fee) basis.

Each of the five names that cleared the screen also carries a live or near-term catalyst — a tokenomics change, a new product, an institutional inflow — that gives a re-rating a reason to happen, rather than relying on the market to notice the discount on its own.

Screening Methodology

Tokens were screened across the TID Research DeFi universe of 35 names using three primary filters:

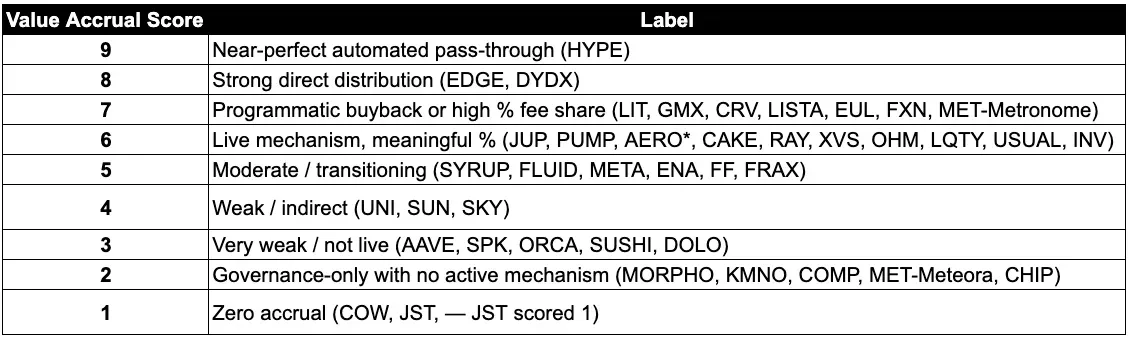

Circulation ratio ≥ 60% — high circ supply limits near-term dilution risk and makes MCap/Fee a more accurate signal than FDV/Fee

Value Accrual Score ≥ 5 (on a 1–9 scale) — the protocol must have a live or near-live mechanism distributing fees to token holders

FDV/12M Fee below sector median — the token must be cheaper than half of its comparable peers on a fee-adjusted basis

Growth-adjusted multiples (FDV/Fee/Growth) and sector-relative 3M and 6M volume or TVL trends were used as secondary signals to identify names with traction rather than purely mean-reversion characteristics. Sector averages and scores were computed from the full 35-name dataset.

Protocol Overview

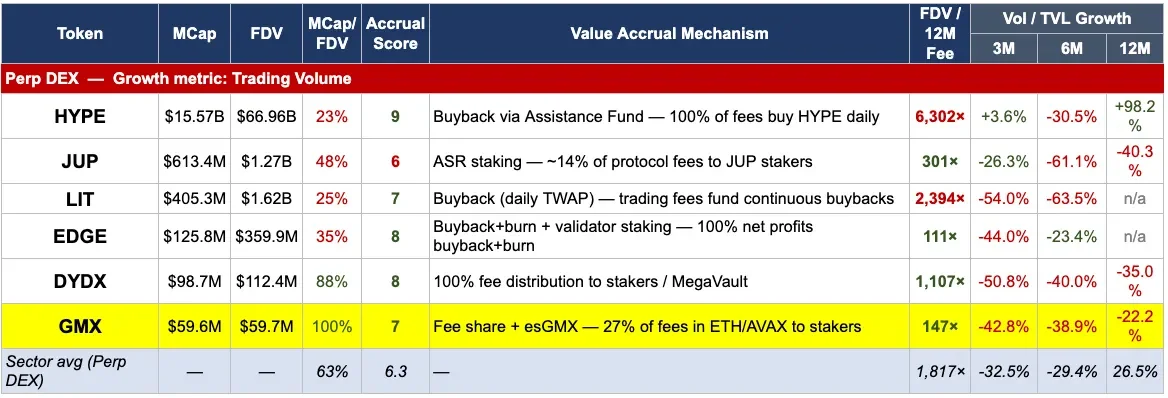

GMX is a decentralised spot and perpetual exchange running on Arbitrum and Avalanche, generating $485 million in lifetime protocol fees since its 2021 launch. It is the only perpetuals DEX in the TID coverage universe at 100% circulation with a fee-to-holder mechanism denominated in native assets (ETH and AVAX), not token emissions.

Value Accrual Mechanism

Stakers receive 27% of all protocol fees in ETH and AVAX directly — not escrowed tokens, not synthetic yields. An additional 10% flows to the treasury, which funds a systematic weekly buyback programme that has been publicly verifiable on-chain since May 2026. The DAO’s March 2026 restructuring replaced direct staking reward emissions with a treasury-directed buyback model, tightening circulating supply and reducing sell pressure. The new Staking Power loyalty mechanism rewards long-duration holders by weighting their share of future buyback distributions by staking duration.

Catalysts

v2.2 / v2.3 upgrade roadmap: gasless transactions via keeper network, multi-chain virtual accounts, cross-collateral support, and a redesigned price impact mechanism — directly addressing barriers to volume recovery

Commodity perpetuals expansion: GMX launched perpetual contracts for gold, silver, WTI crude oil, Brent crude, and natural gas in May 2026 — materially widening its addressable market beyond crypto

Doji partnership (May 2026): GMX is the primary execution venue for Doji, an on-chain proprietary trading platform — a structural source of institutional order flow

MegaETH deployment: GMX launched on MegaETH (10ms block times) in May 2026, adding an eighth network and targeting CEX-competitive execution speeds

GMX as collateral: the token is now accepted as collateral on Radiant Capital’s lending market, adding a new demand layer without supply inflation

Investment Thesis

GMX trades at 147× FDV/Fee against a sector median of 1,817× — a 92% discount — despite being the only fully-diluted perpetuals DEX in the universe with 3+ years of live fee generation.

The March 2026 tokenomics restructuring converts the protocol from an emissions-based reward model to a cash-flow model, removing the primary source of sell pressure.

Volume trajectory is negative across all windows, and the buyback target of $90 per token is aggressive; the valuation discount and supply maturity nonetheless represent a structurally asymmetric setup against a sector that prices early-stage growth into most of its comps.

Protocol Overview

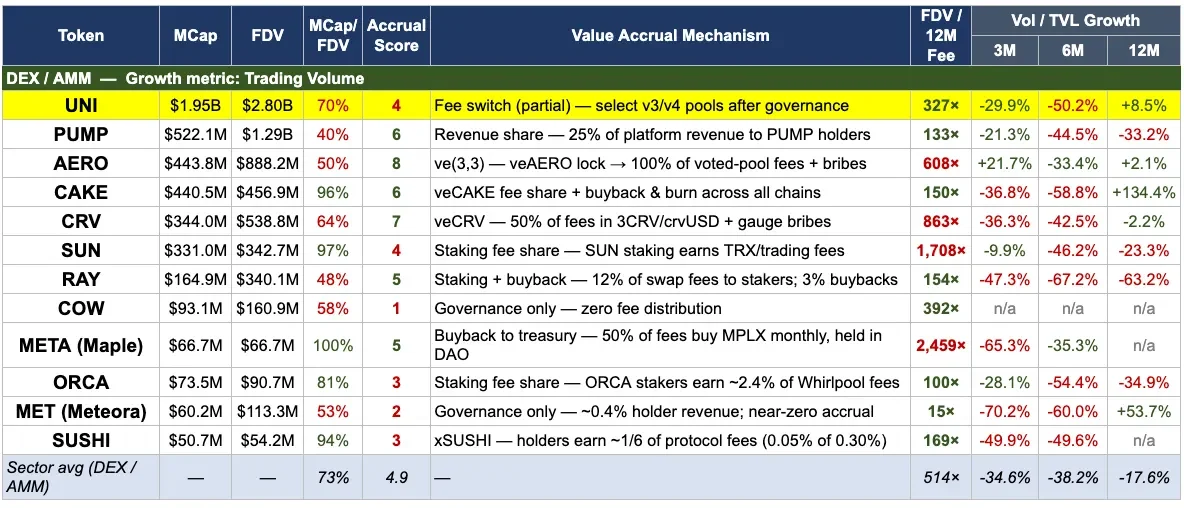

Uniswap is the dominant decentralised exchange by volume and brand recognition, processing hundreds of billions in annual swap volume and powering approximately 31% of MetaMask swaps on mainnet.

Its v4 architecture with programmable hooks and its UniswapX intent-based routing are now attracting both traditional-finance integrations and developer-led liquidity customisation at scale.

Value Accrual Mechanism

The December 2025 UNIfication upgrade activated the protocol fee switch, directing a portion of swap fees from select v3 and v4 pools to buy and burn UNI tokens.

Since activation, 106 million UNI have been burned — 5 million post-switch plus an initial 100 million governance burn — reducing total supply from 1 billion to approximately 895 million. At the current pace of ~1 million UNI per month, the annual burn rate is roughly 1% of remaining supply, a deflationary floor that scales with volume recovery.

Catalysts

Standard Chartered initiation (June 15, 2026): Geoffrey Kendrick, Global Head of Digital Assets Research at Standard Chartered, initiated coverage with a $100 price target by end-2030 — implying ~40× from the $2.50 launch price — with staged milestones of $6.50 by end-2026. The report drove a 20–24% rally, a 4-month high in active addresses, and a 7-month high in whale transactions

Tokenised securities integration: Uniswap now supports trading of tokenised versions of SpaceX, Apple, Tesla, and NVIDIA shares via v4 hooks, building on earlier integrations of BlackRock’s BUIDL fund and Securitize-issued assets. This directly validates Standard Chartered’s thesis that Uniswap will serve as neutral market infrastructure for on-chain real-world assets

Uniswap House (June 24–25, 2026): Two-day community and developer event in New York featuring 32 speakers across v4, hooks, and institutional DeFi — accelerating developer adoption of the v4 hook architecture

BlackRock / Fidelity expansion: Both asset managers expanded tokenised money market fund access via Uniswap protocols in early 2026, with BlackRock reported to be actively accumulating UNI

Investment Thesis

UNI trades at 327× FDV/Fee against a sector median of 514×. The more important signal is the shift in narrative: Uniswap is no longer primarily evaluated as a DEX token but as financial infrastructure.

Standard Chartered’s framework — comparing Uniswap to YouTube and centralised exchanges to Netflix — positions UNI as a beneficiary of the tokenisation supercycle rather than a participant in it.

Volume growth is mixed (3M negative, 12M positive), but the fee switch and 106M burn materially change the supply dynamic. The $6.50 end-2026 target from Standard Chartered implies 120%+ upside from current levels; the valuation multiple gap provides the fundamental anchor for that thesis.

Protocol Overview

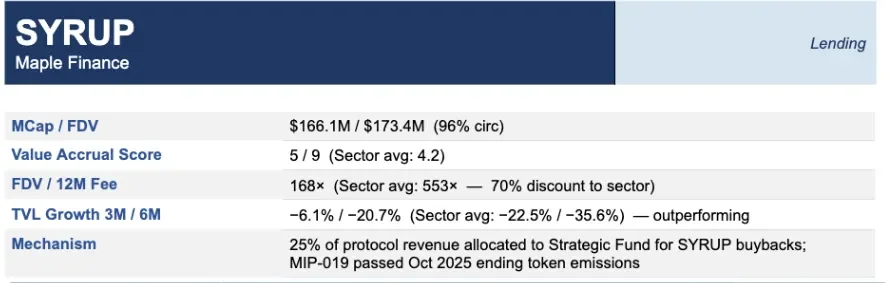

Maple Finance is the leading institutional on-chain credit platform, managing approximately $2B in TVL through overcollateralised lending to vetted institutional borrowers.

Its Syrup.fi consumer arm provides yield-bearing stablecoins (syrupUSDC, syrupUSDT) accessible via Aave integration, effectively channelling idle DeFi capital into institutional credit pools at higher risk-adjusted yields.

Value Accrual Mechanism

MIP-019, passed in October 2025, ended SYRUP token emissions and redirected 25% of all protocol revenue to the Syrup Strategic Fund, which executes systematic open-market SYRUP buybacks.

At current revenue run-rates this represents a price-agnostic, continuous buyer of approximately 2% of circulating supply annually, scaling linearly with protocol revenue growth. The first buyback cycle (April 2026) retired 26.6 million SYRUP for ~$572K. The protocol targets $100M ARR by end-2026, which at 25% allocation would produce ~$25M in annual buyback demand.

Catalysts

syrupBTC launch: A legal dispute with Core Foundation was settled on May 22, 2026, clearing the path for syrupBTC — a Bitcoin yield product that opens a new addressable market for Maple beyond stablecoin strategies

KelpDAO migration tailwind (April 2026): The $292M KelpDAO bridge exploit triggered a DeFi bank run from Aave. Over $2.4B rotated into Spark and Maple within days, with Maple perceived as having tighter risk controls. Justin Sun moved $174M into Spark in the immediate aftermath — this flight-to-safety dynamic directly benefits Maple’s TVL and lending revenue

Revolut listing (April 2026): SYRUP listed on Revolut in the UK and EU, dramatically expanding retail distribution for what had been an institutionally-accessed protocol

Aave strategic partnership (October 2025): Maple’s syrupUSDT and syrupUSDC integrated directly into Aave, routing Aave’s idle capital into Maple pools — a structural, ongoing source of TVL and fee revenue

$100M ARR target: Maple’s founders publicly committed to $100M ARR by end-2026 following record monthly revenue in Q4 2025, providing a clear fundamental milestone

Investment Thesis

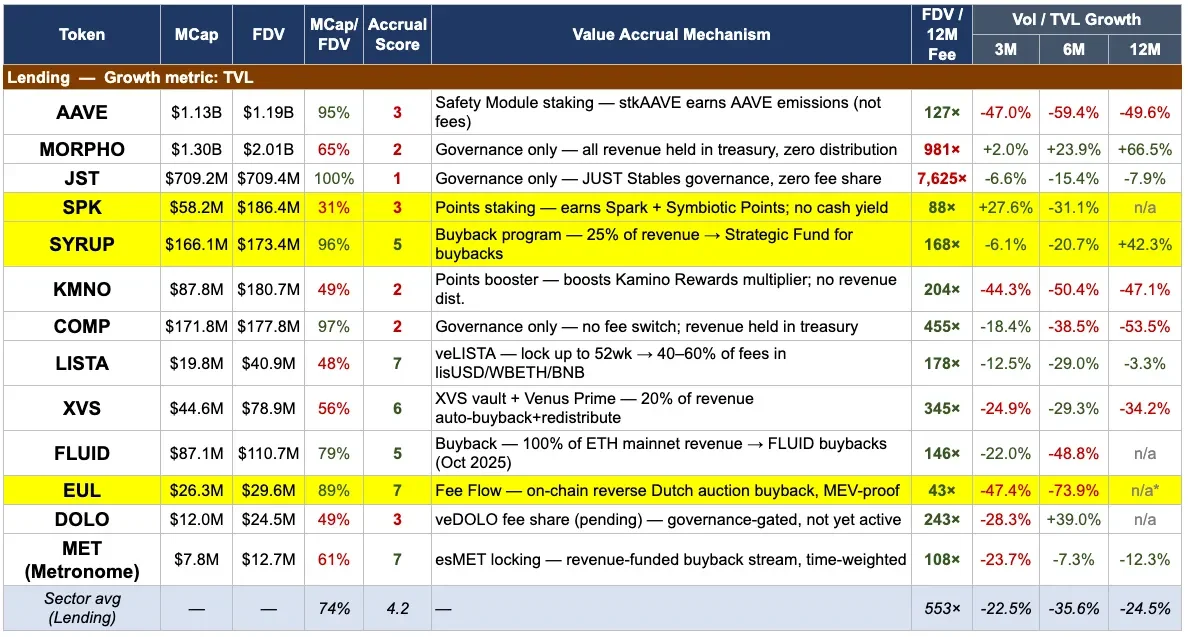

SYRUP trades at 168× FDV/Fee against a sector median of 553×, at 96% circulation, and is outperforming the lending sector on TVL trajectory across every available window (−6.1% vs sector −22.5% at 3M; −20.7% vs −35.6% at 6M).

The MIP-019 switch from emissions to buybacks is structurally analogous to a corporate dividend initiation — it converts a dilutive governance token into a cash-flow capture asset.

The syrupBTC launch and the AUM migration from KelpDAO contagion provide two independent growth catalysts beyond the valuation discount. Key risk: Q1 2026 revenue fell 31% QoQ, indicating sensitivity to the credit cycle; sustained loan demand is required to fund the buyback programme at scale.

Key Risks

Sector-level

DeFi volume recovery remains uncertain — all five tokens are negatively exposed to continued on-chain trading and lending contraction

Regulatory developments around DeFi protocols and tokenised assets in key jurisdictions (EU MiCA, US) could impose compliance costs or restrict addressable markets

Token-specific

GMX: volume recovery is the single gating variable; the $90 buyback price target creates a very long duration for staker reward reinstatement

UNI: the fee switch burn rate (~1% annually) is modest relative to current inflation; tokenised asset volumes flowing through Uniswap are still small relative to the Standard Chartered thesis

SYRUP: Q1 2026 revenue fell 31% QoQ; the buyback programme is contingent on revenue recovery; off-chain underwriting by credit delegates introduces opacity relative to pure on-chain protocols