Fixed-Rate Protocols - The Emerging Certainty of Yields

Early DeFi relied on variable-rate, pool-based models like Aave to bootstrap liquidity. These protocols often suffer from “rate shock”—unpredictable interest spikes that erode profit margins and trigger sudden liquidations.

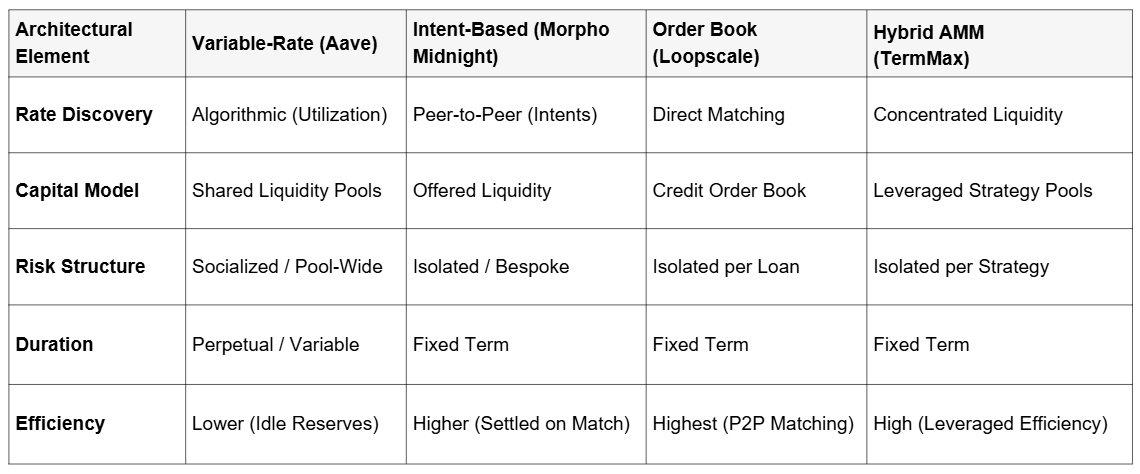

As the ecosystem matures toward institutional-grade infrastructure, a new generation of protocols—Morpho Midnight, Loopscale, and TermMax—is replacing algorithmic volatility with fixed-rate certainty.

By utilising intent-based matching, credit order books, and hybrid AMMs, these platforms provide the predictable cost of capital necessary for sophisticated financial planning and long-term credit expansion.

From Algorithmic Pools to Fixed-Rate Markets

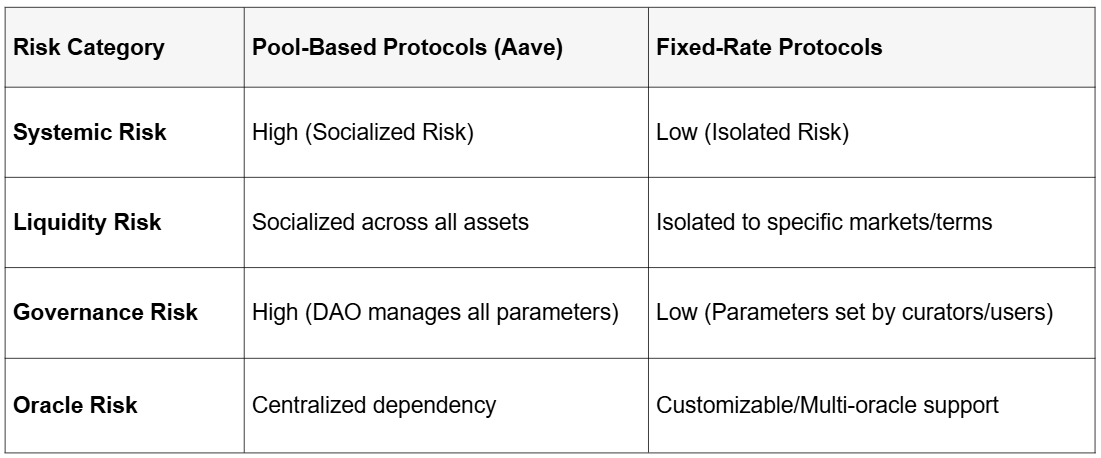

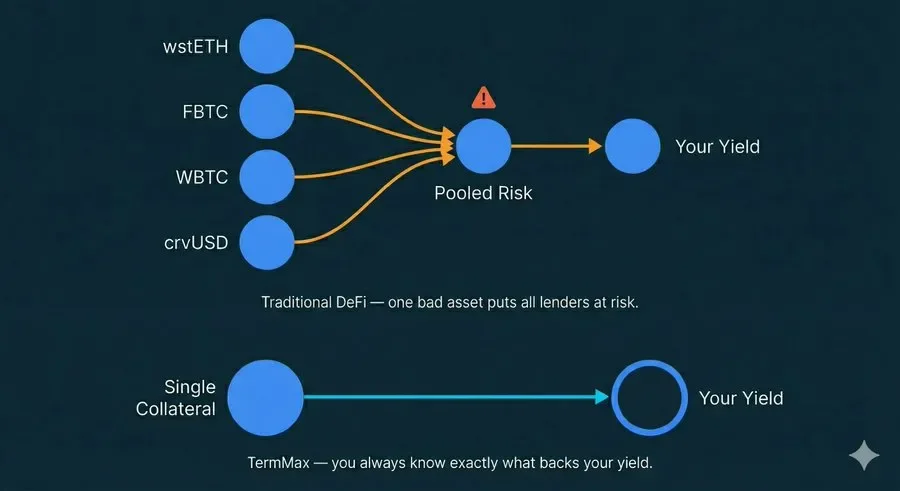

DeFi lending’s “Martian casino” era relied on monolithic pools with socialised risk, exposing lenders to every asset’s vulnerability and subjecting borrowers to unpredictable rate spikes governed by utilisation curves.

Fixed-rate protocols address these inefficiencies by offering a deterministic cost of capital. Morpho Midnight, an evolution of the modular Morpho Blue architecture, shifts the paradigm toward intent-based, fixed-term lending.

Unlike its predecessor, Midnight externalises both risk and rate management to market participants, enabling granular credit pricing and bespoke loan agreements that bypass restrictive, protocol-wide formulas.

Credit Model Comparison

Why Fixed Rates Matter for DeFi Users

The primary appeal of fixed-rate protocols lies in shifting the DeFi experience from speculative volatility to reliable financial planning. For the average user and sophisticated trader alike, these protocols solve three fundamental issues:

1. Eliminating “Rate Shock” and Liquidation Risk

In traditional variable-rate protocols, borrowing costs can spike from 5% to 50% in a single day if demand for an asset surges. For users utilizing leverage, these spikes can instantly turn a profitable strategy into a loss or trigger unexpected liquidations.

Fixed-rate protocols lock in the borrowing cost for the duration of the loan, ensuring that users are insulated from market panic and interest rate volatility.

2. Guaranteed Passive Yield

Lenders in variable-rate pools often see their APY dwindle as more liquidity enters the pool. Fixed-rate protocols allow lenders to secure a “guaranteed” return for a set period.

This is particularly attractive for users seeking predictable income to fund real-world expenses, such as mortgage payments or business operations, where knowing the exact cash flow is essential.

3. Advanced Use Cases

Leverage Amplification via “PT Looping”

Principal Tokens (PT) from protocols like Pendle act as zero-coupon bonds, trading at a discount until they redeem 1:1 at maturity . Users can now provide PT tokens as collateral to borrow at a fixed cost.

By recursively borrowing and buying more PTs—a strategy known as “looping”—users amplify their fixed yield with absolute certainty that their debt interest won’t spike and flip the trade into a loss .

Tenor Matching for RWAs and Private Credit

Tokenized Real-World Assets (RWAs), including treasury bonds and private credit, typically offer fixed returns over defined durations (tenors) . Fixed-rate protocols allow users to borrow against these assets using a matching tenor.

This “locks in” a guaranteed net spread between the RWA’s yield (e.g., 10%) and the fixed borrowing cost (e.g., 6%), insulating the user from the volatility of traditional DeFi money markets.

Corporate Treasury and the Term Structure Curve

Enterprises and protocols increasingly require predictable funding for operations like GPU clusters or trade finance . These entities prioritize risk profiles that match their real-world liabilities. By establishing market-driven yield benchmarks across different durations (e.g., 1-month or 3-month), these protocols are building an on-chain “term structure curve.”

This curve is the essential foundation for pricing future financial derivatives and institutional hedging tools.

Risk Isolation and Liquidation Framework

Morpho Midnight and Loopscale utilize an isolated risk management structure. Each loan is a self-contained agreement, meaning that the failure of a specific collateral type or a default by a particular borrower cannot cause contagion across the protocol. This is particularly relevant for “long-tail” assets and niche LP tokens that may have higher volatility profiles.

The liquidation process on Loopscale is designed to maintain protocol solvency by allowing liquidators to seize collateral at a discount when a borrower’s Loan-to-Value ratio exceeds a defined threshold.

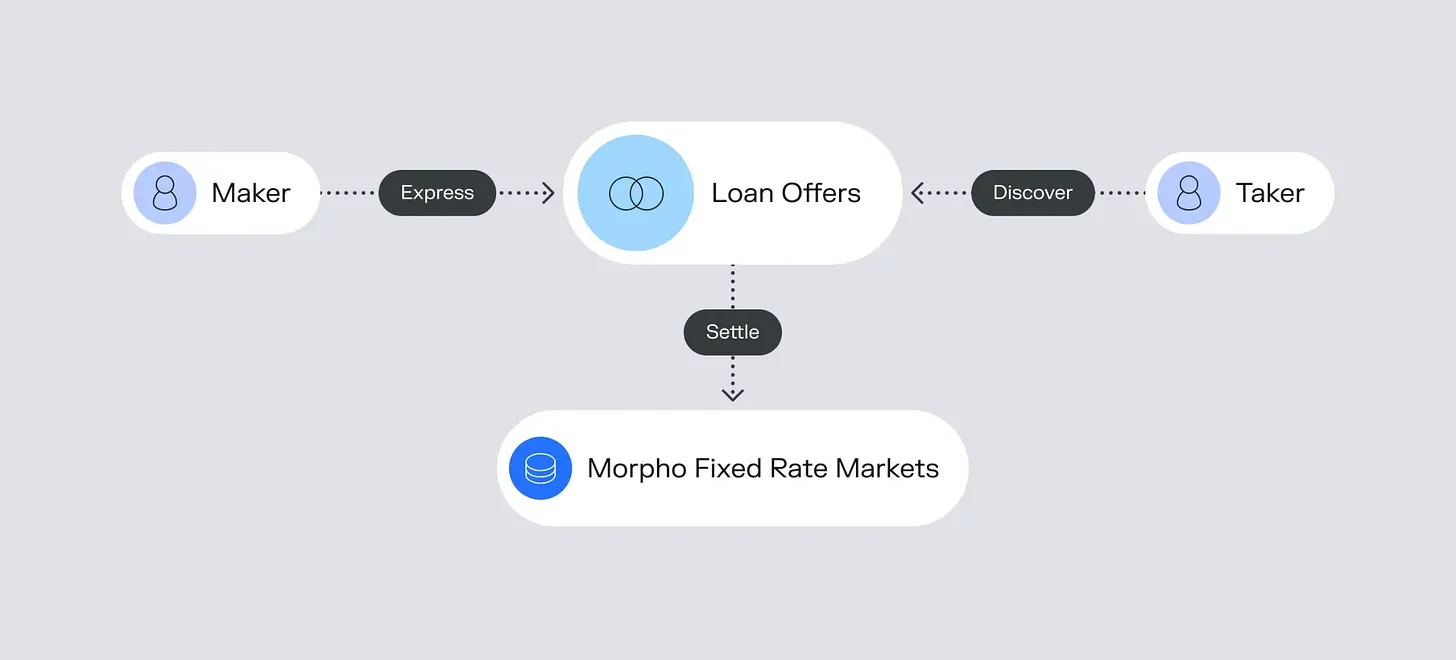

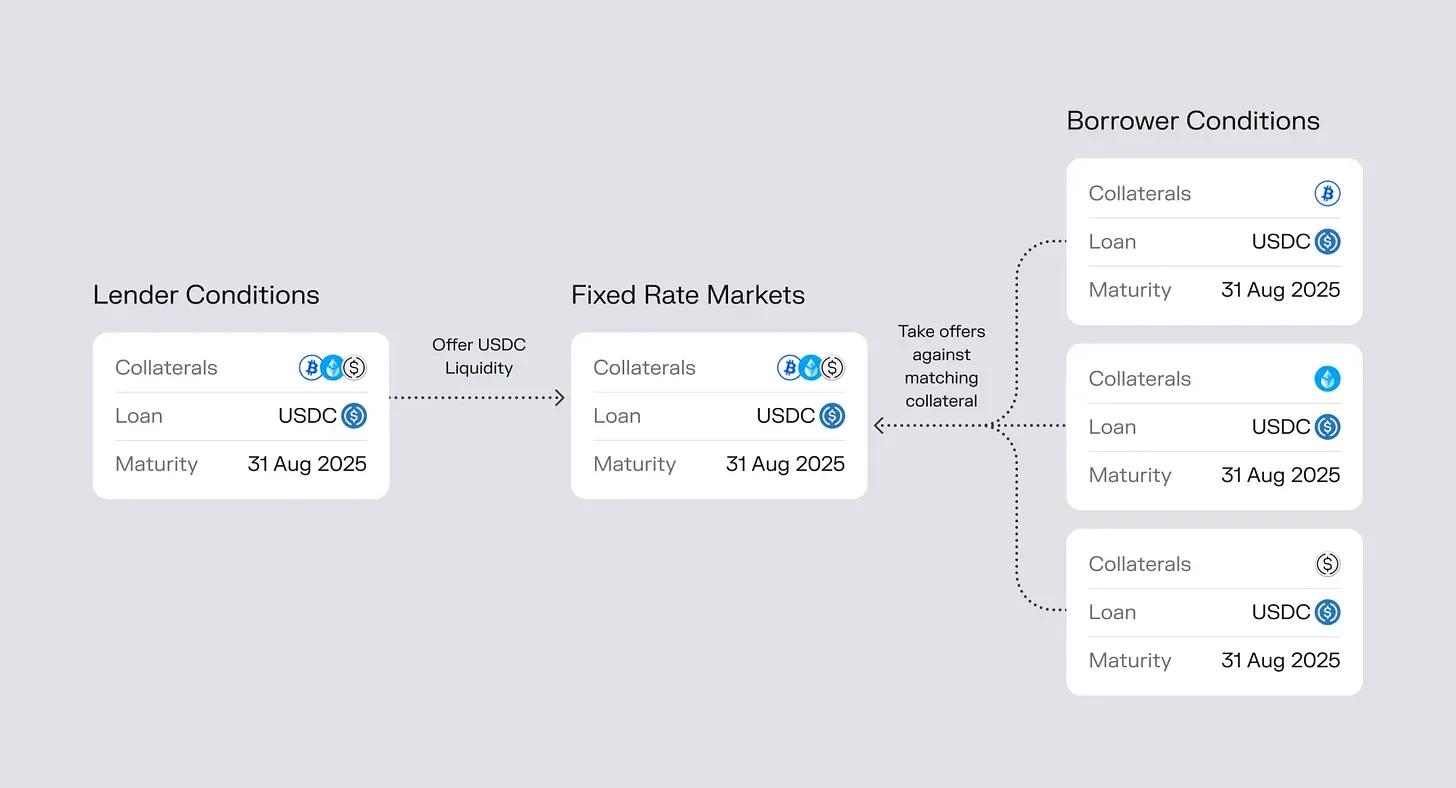

Morpho Midnight: The Mechanics of Offered Liquidity and Intent Settlement

Morpho Midnight represents a fundamental shift away from the pre-allocated capital model that has defined DeFi for years. Midnight introduces the concept of “offered liquidity,” where users broadcast their lending or borrowing intents to a global market without necessarily locking capital into a specific vault until a match occurs.

Intent-Based Matching and Bespoke Terms

Lenders can express complex intents that specify multiple conditions simultaneously. For instance, a single lender can offer USDC liquidity against a variety of collateral assets—ranging from blue-chip tokens like ETH to niche liquid staking tokens (LSTs) or even tokenized real-world assets (RWAs)—while specifying different interest rates and Loan-to-Value (LLTV) ratios for each.

This flexibility is achieved through externalized management of both risk and rates. Curators and sophisticated allocators can actively price risk and set competitive rates, ensuring that the cost of borrowing accurately reflects real-time supply and demand rather than an arbitrary mathematical curve. Furthermore, Midnight supports cross-chain settlement, where the chain on which the loan is settled becomes a parameter of the offer. A lender could offer USDC liquidity across Ethereum, Base, and OP Mainnet simultaneously, and the borrower determines the final settlement chain.

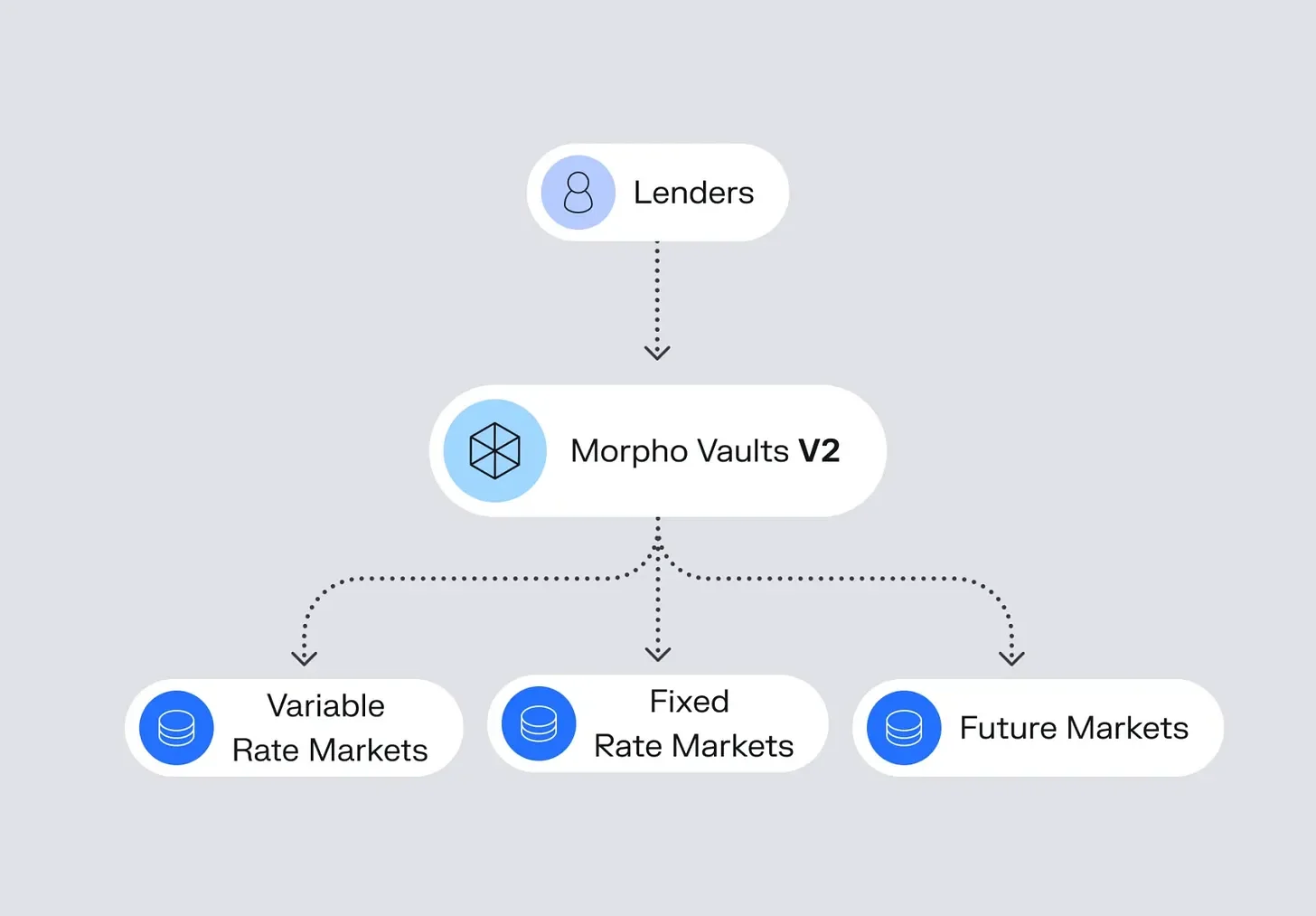

Synergistic Utility with Morpho Blue

The relationship between Morpho Blue and Morpho Midnight is complementary rather than competitive. Morpho Blue provides the immutable, permissionless infrastructure for variable-rate markets, while Midnight offers the tools for fixed-term predictability. Users can leverage Morpho Vaults (MetaMorpho) to earn variable yields while their “intents” are waiting to be matched in the Midnight fixed-rate market, ensuring that their capital remains productive at all times.

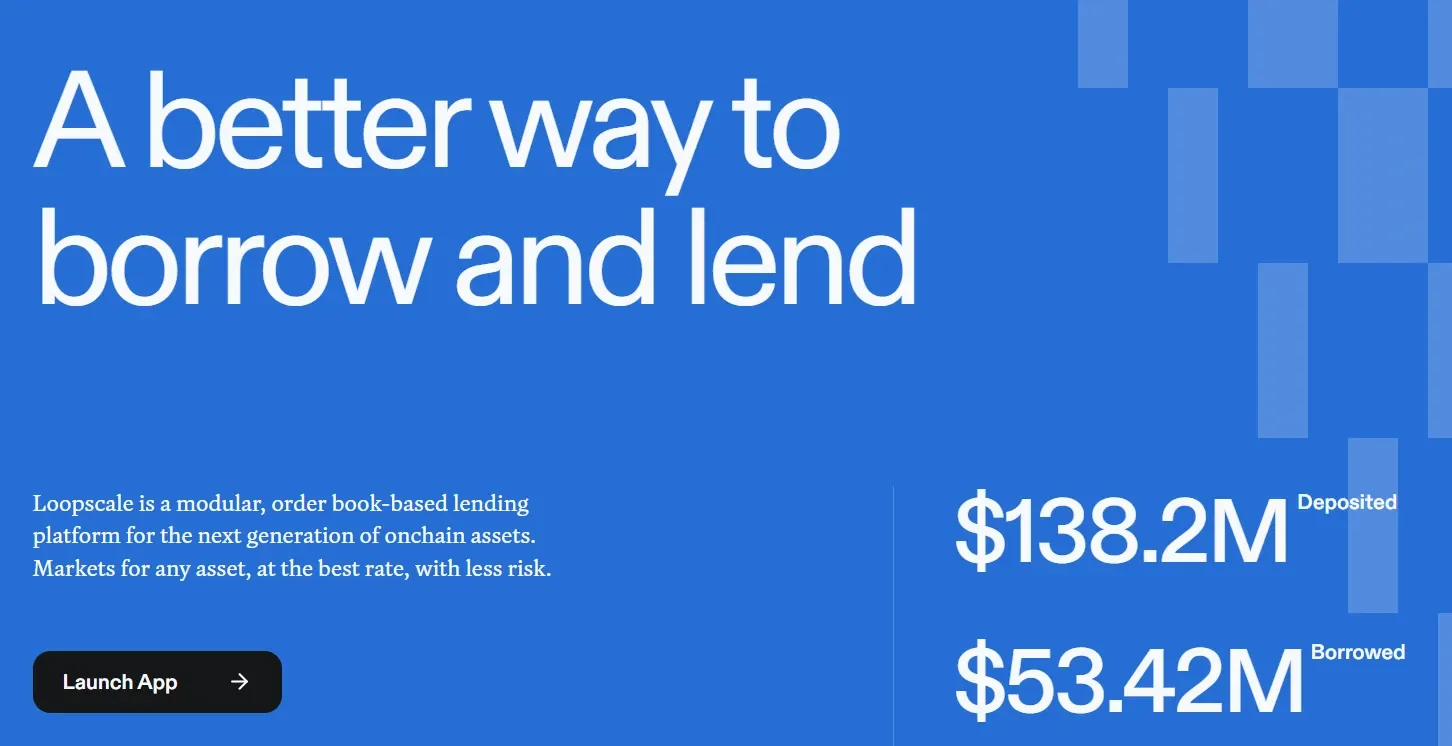

Loopscale: High-Performance Credit Order Books on Solana

Loopscale’s Credit Order Book (COB) replaces the traditional AMM-based liquidity pools with a direct market-matching system akin to centralized exchanges.

The Zero-Spread Efficiency Model

One of the primary innovations of Loopscale is the elimination of the interest rate spread. In pooled models, the rate paid by borrowers is always significantly higher than the rate received by lenders to account for idle capital and protocol fees. Because Loopscale uses an order book to match individual lenders and borrowers directly, the lend rate is equal to the borrow rate. This creates a more equitable environment for both participants: lenders achieve higher yields because their capital is fully utilized, and borrowers benefit from lower costs.

Product Stack and User Flows

Loopscale partitions its offerings into three distinct categories to serve different user personas and intents:

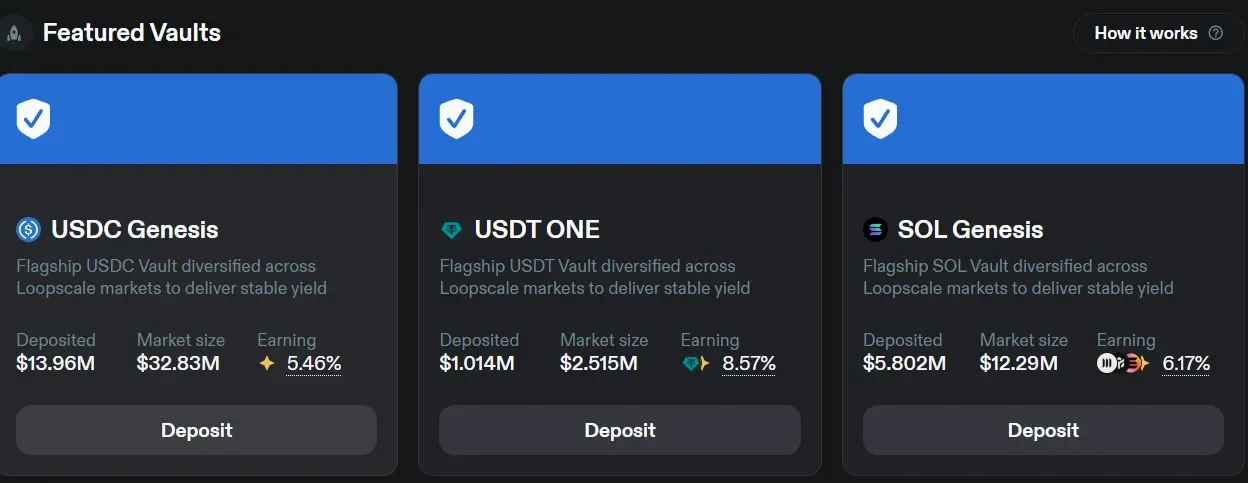

Loopscale Vaults: Designed for passive lenders, these vaults are managed by curators who allocate capital across the protocol’s fixed-rate markets. The vaults utilize an “Optimized Liquidity” feature, where any capital not currently matched in a fixed-term loan is deployed to external variable-rate protocols like MarginFi to maintain yield continuity.

Advanced Lending: This interface provides power users with the ability to set granular terms for their loans. Lenders can specify the exact asset, interest rate, duration, and collateral types they are willing to accept. This peer-to-peer approach allows for the dynamic pricing of idiosyncratic risks.

Loops (One-Click Leverage): Leveraging the fixed-rate nature of the protocol, Loopscale offers “Loops,” which allow users to amplify their exposure to yield-bearing assets. A user can deposit stSOL, borrow more stSOL at a fixed rate, and redeposit it to multiply their staking rewards. Because the borrowing cost is fixed for the duration of the loop, the user is insulated from the risk of a rate spike that could render the strategy unprofitable.

TermMax: Hybrid AMM Models and Yield Token Integration

TermMax introduces a specialized architecture that blends fixed-rate lending with automated leveraged strategies. The protocol is designed to simplify complex yield operations and establish a standardized yield curve for on-chain assets.

Customized AMM Interest Rate Order Book

The core of TermMax is a hybrid matching engine that utilizes a modified version of the Uniswap V3 concentrated liquidity model. Instead of providing liquidity across a price range, market makers on TermMax provide “range interest rate quotes”. This allows them to concentrate their capital at specific interest rate levels for different durations, providing deeper liquidity and more accurate pricing for fixed-term debt.

Strategic Use of Yield-Bearing Tokens

TermMax distinguishes itself by its deep integration with yield-bearing assets, specifically Principal Tokens (PT) from Pendle. By allowing these tokens to be used as collateral for fixed-rate loans, TermMax enables “Return Amplification”. Users can borrow against their PT tokens at a fixed cost that is lower than the inherent yield of the token, creating a risk-defined leveraged yield position.

Risks and Structural Disadvantages

While fixed rates provide predictability, they introduce specific trade-offs and risks not found in variable-rate “on-demand” money markets:

Opportunity Cost and “Maturity Lock”: Locking in a fixed rate is a double-edged sword. If a borrower locks in a 10% rate and market interest rates subsequently fall to 5%, the borrower is stuck paying significantly more than the current market value. Conversely, lenders might miss out on yield spikes if they lock funds at a low rate before a market surge.

Liquidity Fragmentation: In variable protocols like Aave, all liquidity is concentrated in a single pool. Fixed-rate protocols create separate “term segments”—each maturity date is effectively a different financial instrument. This can lead to fragmented liquidity where certain dates have thin depth, making it difficult for large traders to enter or exit without significant slippage.

Early Exit Penalties: Unlike variable pools that allow instant withdrawals, fixed-rate protocols usually require lenders to wait until maturity. Exiting early often requires selling the loan position on a secondary market; if liquidity is low, the seller may be forced to accept a steep discount that consumes their expected returns.

Curator and Management Risk: Modular protocols like Morpho or Loopscale rely on external curators to set risk parameters (LTVs, oracles, etc.). Users are exposed to “curator risk,” where poor management decisions or a lack of technical oversight can lead to bad debt or protocol revenue loss.

Negative Carry Mismatch: For looping strategies, if the cost of the fixed borrowing rate exceeds the underlying asset’s yield (e.g., if an LST’s rewards drop unexpectedly), the position becomes a “negative carry” trade, losing money every day it remains open.

Future Outlook: The Maturation of On-chain Credit

As the DeFi ecosystem evolves, the boundary between money markets and interest rate markets will continue to blur. Interest rate markets, led by protocols like Pendle and the fixed-rate architectures discussed in this report, will become as fundamental as spot exchanges.

The ability for lenders and borrowers to set their own terms, externalize risk management, and access fixed-rate financing for bespoke durations will unlock trillions in volume. Morpho Midnight’s vision of becoming the “financial infrastructure for enterprises” suggests a future where DeFi protocols are the backbone of global debt markets, offering transparency, efficiency, and predictability that traditional banking systems cannot match.

For users, the primary utility of these features lies in the transformation of “idle holdings into productive assets” with defined risk profiles. Whether through the passive yield of Loopscale Vaults, the strategic leverage of TermMax, or the institutional-grade compliance of Morpho Midnight, the tools for sophisticated on-chain capital management have arrived, marking the transition from speculative experiment to a durable, recognisable financial system.