Guide to Low-Risk Yield-Bearing Stablecoins

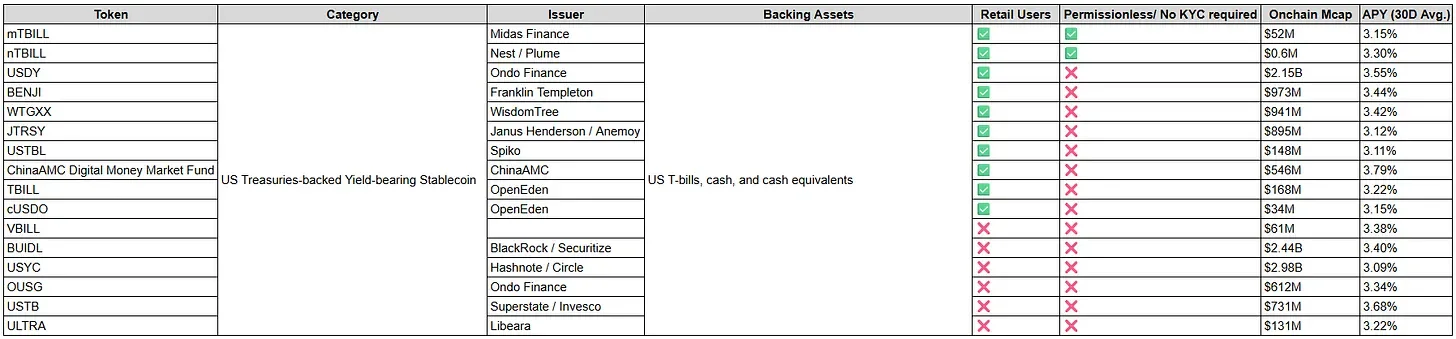

1. US Treasuries-Backed Yield-Bearing Stablecoins

These stablecoins are strictly backed by US T-bills, cash, and cash equivalents. They are designed to mirror traditional money market funds, passing the “risk-free” rate of the US government directly to token holders.

The following options are accessible to retail investors, divided into permissionless assets and those requiring platform KYC. (Note: Institutional-only options like BUIDL, USYC, OUSG, USTB, ULTRA, and VBILL have been omitted).

Permissionless & No KYC Required

These tokens can be freely bought, sold, and held onchain without passing through a centralized compliance gateway.

Onchain Market Cap: $53M

30D Avg. APY: 3.15%

Retail-Accessible (Requires Platform KYC)

These issuers require users to create an account and pass identity verification to mint or redeem the asset directly, though they can often be traded on secondary decentralized markets.

Onchain Market Cap: $2.15B

30D Avg. APY: 3.55%

2. Credit-Backed Yield-Bearing Stablecoins

Credit-backed stablecoins represent the intersection of TradFi and DeFi. Rather than relying on government debt, these assets generate yield by facilitating loans to real-world businesses, institutions, or homeowners. While the yields are highly attractive, investors must swap standard interest rate risk for counterparty and credit risk.

syrupUSDC & syrupUSDT (Maple Finance)

Backing: Private corporate and institutional credit loans.

How Yield is Generated: Maple Finance operates decentralized lending pools where whitelisted institutional borrowers (such as market makers, trading firms, and fintechs) take out short-to-medium-term loans. The interest these institutions pay to access capital is aggregated and passed on to retail users holding the “Syrup” receipt tokens.

The Risk Profile: The primary risk here is default contagion. If a major institutional borrower goes bankrupt and cannot repay their loan, the lending pool takes a haircut, directly impacting the value of the syrup tokens.

Metrics: $1.38B Mcap (USDC) at 4.83% APY / $381M Mcap (USDT) at 4.35% APY.

Backing: Home Equity Lines of Credit (HELOC).

How Yield is Generated: This model tokenizes physical real estate debt. Real-world homeowners take out loans against the equity in their houses. As these homeowners make their monthly interest payments, the cash flow is tokenized and distributed to PRIME token holders onchain.

The Risk Profile: PRIME introduces real estate market exposure. While the loans are backed by hard assets (homes), a severe housing market downturn could lead to widespread foreclosures. Additionally, there is an “oracle and bridging risk” required to seamlessly link real-world home deeds to onchain token cash flows.

Metrics: $375M Mcap at 6.62% APY.

3. DeFi-Native Yield-Bearing Stablecoins

Unlike credit-backed assets that look to the real world for yield, DeFi-native stablecoins generate returns directly from the blockchain economy. These assets rely on over-collateralization, decentralized lending markets, and automated trading strategies. The primary risks here shift from corporate defaults to software bugs, market liquidity crises, and algorithmic de-pegging.

Backing: The Spark Liquidity Layer, Grove Portfolio, and Obex Investments (a hybrid of crypto-collateral and tokenized Real World Assets).

How Yield is Generated: Users lock USDS into a savings module to receive sUSDS. The Sky protocol generates massive revenue by charging borrowers fees to mint stablecoins and by earning interest on its treasury. This revenue is redirected directly into the savings rate paid to sUSDS holders.

The Risk Profile: sUSDS carries governance and complexity risk. The yield rate is actively managed and voted on by decentralized governance, meaning APYs can fluctuate.

Metrics: $6.54B TVL at 3.60% APY.

sGHO (Aave)

Backing: A massive, diverse basket of crypto and Real World Asset collaterals deposited into the Aave lending protocol to mint the underlying GHO.

How Yield is Generated: GHO is Aave’s native, overcollateralized stablecoin. Users who deposit GHO into the “Savings GHO” (sGHO) smart contract receive a dynamic yield. This yield is clean and protocol-native—funded directly by the interest borrowers pay to mint GHO on Aave, alongside DAO-directed governance rewards.

The Risk Profile: sGHO operates as a highly liquid, non-custodial savings account. Crucially, sGHO holders face no slashing risk (Aave’s protocol insurance and bad-debt risk are handled separately by advanced users in the automated “Umbrella Module”). The primary risks for sGHO are smart contract risk (bugs in Aave’s code) and peg risk (extreme market volatility causing temporary deviations from $1).

Metrics: $126M TVL at 4.25% APY.

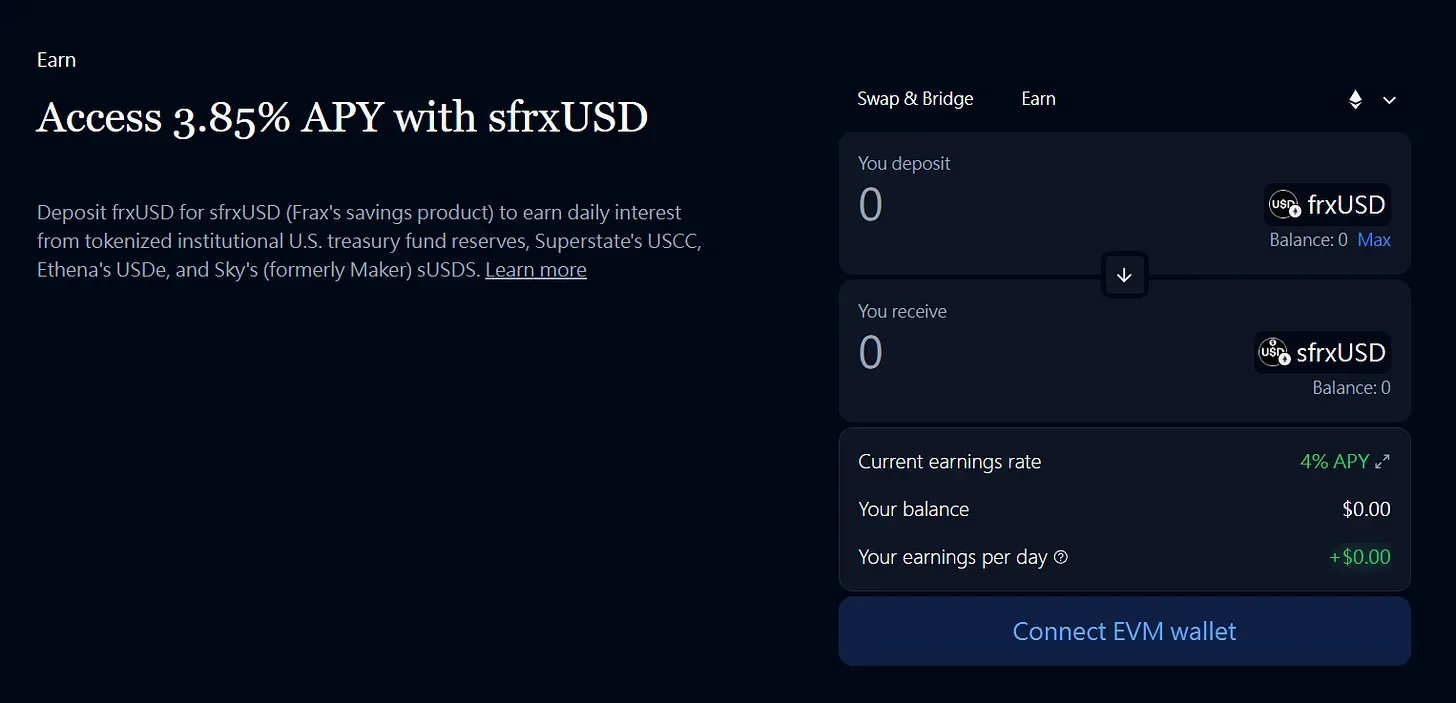

sfrxUSD (Frax Finance)

Backing: Multi-DeFi Yield Strategies driven by Algorithmic Market Operations (AMOs).

How Yield is Generated: Frax deploys its treasury into various decentralized yield strategies—such as providing liquidity on decentralized exchanges or supplying capital to lending markets—via automated smart contracts known as AMOs. The trading fees and interest accrued by these AMOs are continuously routed back to users who stake their frxUSD to hold sfrxUSD.

The Risk Profile: This asset is highly exposed to composability risk. Because Frax’s AMOs plug into external protocols to generate yield, an exploit in any of those connected protocols could impact Frax’s funds.

Metrics: $32.6M TVL at 4.05% APY.

4. GENIUS Framework Stablecoins

These are core stablecoins generally backed by high-quality assets (primarily US T-bills, cash, and cash equivalents) that do not natively compound yield directly into the token itself. Instead, issuers distribute yield externally through liquidity incentives, farming rewards, and ecosystem campaigns.

Important Risk Warning: Because the stablecoins themselves do not generate yield passively in your wallet, you must actively deploy them into third-party decentralized lending markets and yield farms. While the underlying stablecoin may be low-risk, routing them into external pools introduces smart contract risk (vulnerabilities in the lending protocol code), curator/manager risk (if the pool is managed by a third party), and liquidity risk (the ability to withdraw your funds during peak congestion).

For investors comfortable with interacting directly with DeFi protocols, the following incentivized farming strategies currently exist for GENIUS framework stablecoins:

PYUSD (Paypal)

Onchain Market Cap: $3.24B

Target APY Range: 4.5% – 5.0%

Farming Strategy: Users can supply PYUSD to low-risk lending pools on Euler and Morpho. These specific pools are curated by Sentora and are directly incentivized by PayPal with additional PYUSD rewards.

Onchain Market Cap: $1.75B

Target APY Range: 4.0% – 5.0%

Farming Strategy: Users can supply RLUSD to lending pools on Morpho, curated by Sentora, or a dedicated lending pool on Aave V3, which are both incentivized by Ripple with RLUSD rewards.

Follow @todayindefi to keep up with the latest DeFi news on Twitter.

Disclaimer: Projects or tokens mentioned in this newsletter are often experimental or unaudited. Do your own diligence before using or buying anything mentioned.