What is strategy’s $sTRC

What Most People Are Missing About Strategy's Most Important Instrument

Most of the coverage on Strategy focuses on Bitcoin price and Michael Saylor's Twitter activity. That's the wrong place to look. The real story is a financial engineering instrument that most retail investors don't understand at all, and that even institutional observers have underestimated. It is called STRC — and in the past week alone, it funded 75% of a $1.57 billion Bitcoin purchase, the largest single-week buy Strategy has made in 2026.

Let’s walk through exactly what it is, why they built it, when it happened, what the actual risks are, and what the data tells us about its relationship to Bitcoin's price.

I. How $STRC Works

STRC — marketed under the name "Stretch" — is Strategy's perpetual preferred stock that currently pays 11.50% annual dividends, payable monthly in cash. Its dividend rate is adjusted monthly to encourage trading around its $100 par value and to help strip away price volatility.

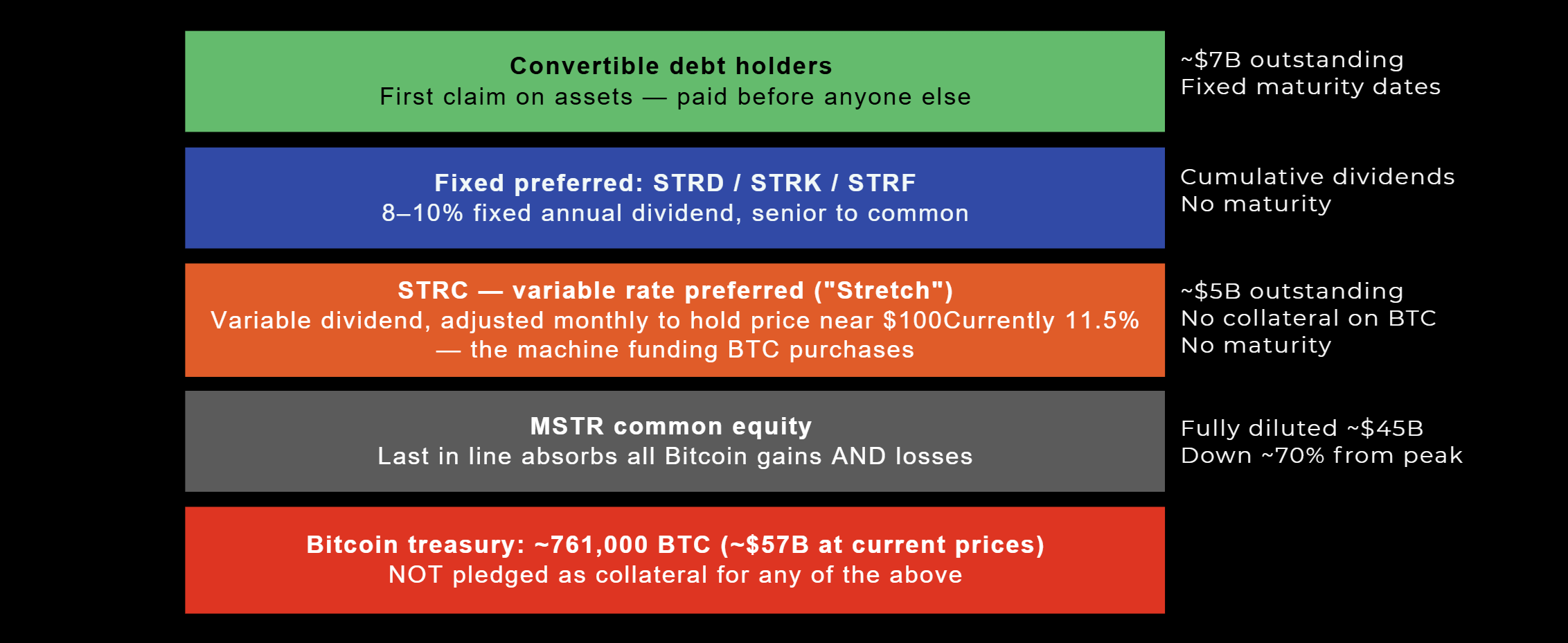

The first diagram above shows exactly where STRC sits in Strategy's capital structure. The key thing to understand is the priority ladder: debt holders sit at the top, then fixed preferred (STRD, STRK, STRF), then STRC, then common equity (MSTR shares) at the very bottom. This matters enormously when we get to risks.

STRC is not a Bitcoin ETF. It is not a bond. It is not a savings account. It is a perpetual preferred security — meaning it never matures, never forces Strategy to return your principal, and pays you a variable dividend rate that the company controls monthly at its own discretion. You are providing permanent capital in exchange for an income stream that can be raised or lowered.

The economic logic of STRC for Strategy is elegant. Strategy sells $100K of STRC, yielding 11%, and buys 1 BTC at $100K. It now has an annual dividend obligation of $11,000. Five years pass; Bitcoin rises to $1 million. Strategy now holds $1 million of BTC, but has paid $55,000 to service the STRC dividend. That's an $845K gain to MSTR shareholders.

This is the bet Saylor is making. If Bitcoin significantly outperforms the 11.5% dividend cost — which he believes it will — MSTR common shareholders are massively enriched. STRC holders receive their fixed yield but capture none of the upside above that rate.

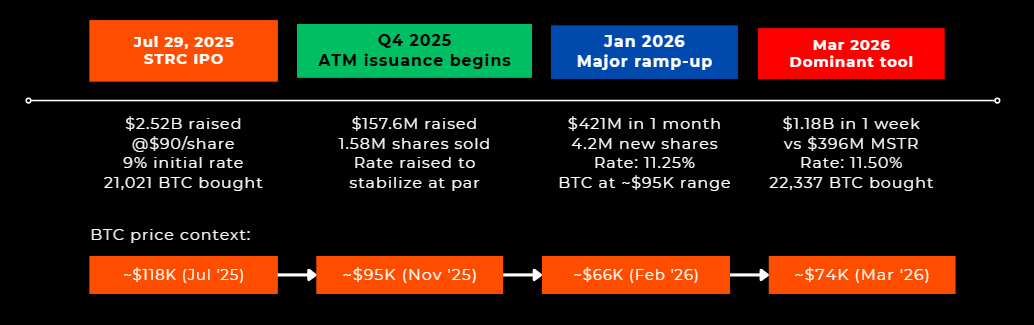

II. The Timeline

The timeline diagram above captures the key inflection points.

III. Why They Built It — The Strategic Logic

To understand STRC, you have to understand the problem Strategy faced by mid-2025. When Strategy's shares peaked in the summer of 2025, the accretion-via-dilution approach had raised the coins held for each 1,000 shares from 1.5 at the end of 2023 to 2.12, a rise of 41%. That worked beautifully when the stock traded at a massive premium to its Bitcoin NAV. Selling overpriced shares to buy "underpriced" Bitcoin was a genuine value transfer to shareholders.

Then Bitcoin fell. Strategy shares have fallen 72% from $457 to $130, far faster than Bitcoin's 51% tumble from $129 to $68. Fortune When the stock trades near or below its Bitcoin NAV, the accretion game breaks. Every common share sale now dilutes rather than enriches existing shareholders.

STRC is the solution. Common equity may be used more selectively, primarily when mNAV (multiple to net asset value) is meaningfully above 1. This suggests reduced reliance on common stock sales, while leaning more heavily on STRC, which avoids issuing new common shares. In other words: STRC lets Strategy keep buying Bitcoin without further wrecking the per-share Bitcoin exposure of MSTR holders.

The variable rate mechanism is particularly clever. When STRC trades above $100, Strategy issues more shares via ATM — effectively selling at a premium and pocketing the difference. When STRC dips below $100, Strategy raises the dividend rate to attract buyers back. This creates a self-correcting instrument that, so long as confidence holds, stays anchored near par. According to Saylor, STRC's ATM issuance has averaged about 3.5 times the natural supply of Bitcoin, indicating strong demand relative to BTC's limited supply.

IV. The Risks — This Is What Should Concern You Most

Here is where I must be blunt, and where much of the retail enthusiasm needs a cold dose of institutional analysis.

Risk 1: STRC is not collateralized by Bitcoin.

This is the most misunderstood feature of the instrument. The company's preferred securities (STRF, STRC, STRE, STRK, STRD) are not collateralized by the company's bitcoin holdings and only have a preferred claim on the residual assets of the company. strategy If Strategy's Bitcoin holdings were liquidated, you'd first pay off debt holders, then potentially other obligations. Your claim as a preferred holder is on whatever residual corporate assets exist — not on the Bitcoin itself. This is not a Bitcoin-backed yield product.

Risk 2: The machine requires two simultaneous conditions.

The model requires both STRC to remain near its target price and Strategy's equity to trade at a premium to net asset value — conditions that are largely sentiment-driven and could deteriorate simultaneously in weaker markets. This is the K33 Research warning that deserves serious attention. There is no independent mechanical guarantee here. This is a confidence game, executed by a company with extraordinary Bitcoin exposure. If sentiment breaks on either MSTR common or on STRC itself, both can unravel together.

Risk 3: STRC has already broken par multiple times.

This is not hypothetical. STRC is designed to trade close to its $100 par value, but a loss of confidence in the company, bitcoin, or the preferred shares themselves could push the price below par and cause significant damage. STRC has on several occasions traded below its $100 par value, prompting the company to raise the dividend to help push the shares back toward par. Most recently: the preferred has spent three consecutive days trading below its $100 par value following its March 15 ex-dividend date.

Risk 4: Dividend obligations now exceed $1 billion annually.

At STRC's current 11.5% dividend rate, the $1.18 billion issuance implies roughly $135 million in annual dividend obligations. This has pushed the company's total annual dividend burden above $1 billion. Strategy holds approximately $2.25 billion in cash reserves — that's about 25 months of coverage at current rates. The buffer exists, but it is finite, and every new STRC issuance enlarges the fixed cost base permanently.

Risk 5: The yield far exceeds risk-free rates for a reason.

Two Prime CEO Alexander Blume warns there is "no free lunch," saying yields far above Treasuries imply added risk. An 11.5% yield when 10-year Treasuries yield roughly 4.5% implies the market is pricing in substantial additional risk — Bitcoin collapse risk, company solvency risk, or confidence risk in the instrument itself. If you're buying STRC thinking it's a "high yield savings account," you are mispricing what you own.

Risk 6: If STRC loses its par-anchoring dynamic, the whole capital structure weakens.

If STRC trades below its target level for a prolonged period, confidence in its "return to par" dynamic could weaken, shifting its behavior from a perceived stable yield product toward a more credit-like risk profile. At that point, Strategy can no longer efficiently issue new shares via ATM. Bitcoin purchases stop. MSTR common stock loses its premium. The entire flywheel reverses. This is the tail risk that matters.

V. Is There a Confluence Between STRC Issuances and Bitcoin's Price?

The surface-level intuition is yes: STRC issuances → capital raised → Bitcoin purchased → price supported. In stronger markets, the mechanism creates a feedback loop in which capital raised through STRC issuance supports continued bitcoin buying. When the instrument trades near its target level, Strategy can issue new shares and deploy proceeds into BTC, often alongside common equity issuance.

The data from March 2026 partially supports this. Strategy has spent over $7 billion on Bitcoin already in 2026, with more than half of that in March. That would place it in Strategy's top five of all-time monthly spending. dlnews Over the same period, Bitcoin rose from approximately $66,000 to around $74,000 — a 13% gain. However, attributing that move entirely to Strategy's buying would be simplistic. Multiple factors drove that recovery, including ETF inflows and macro shifts.

The correlation between STRC issuance and Bitcoin price is better described as circular rather than directional. STRC issuances happen most heavily when STRC trades near or above par — which tends to happen when Bitcoin sentiment is improving. Strategy then buys Bitcoin, which further improves sentiment. This is a momentum amplifier, not a price floor. It works powerfully in the upswing and can accelerate the downswing when it breaks.

There is also a counterintuitive observation in the data: Strategy spent just $231 million total during the entire 2022 bear market when Bitcoin prices collapsed below $20,000. Without STRC in 2022, Strategy was constrained. With STRC in 2026, Strategy is buying aggressively through a 40% correction. Whether that constitutes "supporting" the price or merely "buying the dip" is a debate — the scale of the purchases is real either way.

The honest answer: STRC-funded buying does create real Bitcoin demand — Strategy is buying 99% of all corporate Bitcoin treasury purchases these days. But STRC cannot and does not create a price floor. Bitcoin drives STRC viability, not the other way around.

VI. What This Means for Each Type of Investor

If you are considering buying STRC: You are buying a high-yield perpetual preferred issued by a leveraged Bitcoin holding company with no maturity and no collateral on the underlying asset. The 11.5% rate compensates you for Bitcoin risk, MSTR solvency risk, and the instrument's own confidence risk. It is not a bond substitute. It is not cash-equivalent. The $2.25B reserve is real, but finite. Price it accordingly.

If you hold MSTR common: STRC is your best friend in a bear market — it funds Bitcoin accumulation without diluting your per-share Bitcoin exposure. But the growing dividend burden ($1B+ annually) is a permanent structural cost. If Bitcoin stays range-bound, this cost slowly erodes Strategy's ability to maintain reserves.

If you are watching Bitcoin markets: Strategy's STRC machine is the largest single source of new corporate Bitcoin demand in the world right now. Strategy is "playing in its own stadium right now," especially as corporate treasury purchases have outpaced global exchange-traded product buys by a wide margin. Any deterioration in STRC's ability to raise capital would meaningfully reduce a genuine marginal buyer in the market.

The machine is impressive. It is also, by design, built on confidence. And confidence, as every institutional trader knows, is the most fragile input of all.

This is a research note for informational purposes. It does not constitute investment advice. All figures sourced from Strategy's official press releases, SEC filings, and third-party institutional research from K33, Bitwise, and CoinDesk as of March 2026.