Best Low Risk DeFi Stablecoin Yields

Not every yield in DeFi requires degen-level risk. There's a growing ecosystem of battle-tested protocols where you can park stablecoins and earn meaningful returns — without touching leverage, volatile tokens, or unaudited contracts.

This guide breaks down the major categories of stablecoin yield in DeFi, explains where each yield actually comes from (because if you can't explain it, you're the yield), and helps you decide which fits your risk profile.

We're only covering proven, large-TVL protocols that have survived market cycles or demonstrated strong institutional adoption. No farms with anonymous teams and 500% APY.

The Five Categories of Stablecoin Yield

Before diving into specific protocols, it helps to understand that not all "stablecoin yield" is the same. The source of the yield determines the risk profile. We break them into five categories:

Savings Rate Protocols — Yield from protocol revenue (loans, treasury bills)

Lending Markets — Yield from borrowers paying interest

Incentivized Lending — Temporary boosted yields from token rewards or promotional programs

Institutional Private Credit — Yield from overcollateralized loans to vetted institutions

RWA-Backed Yield: Tokenized Treasuries On-Chain

Basis Trade / Delta-Neutral — Yield from funding rates on perpetual futures

Let's go through each.

1. Savings Rate Protocols

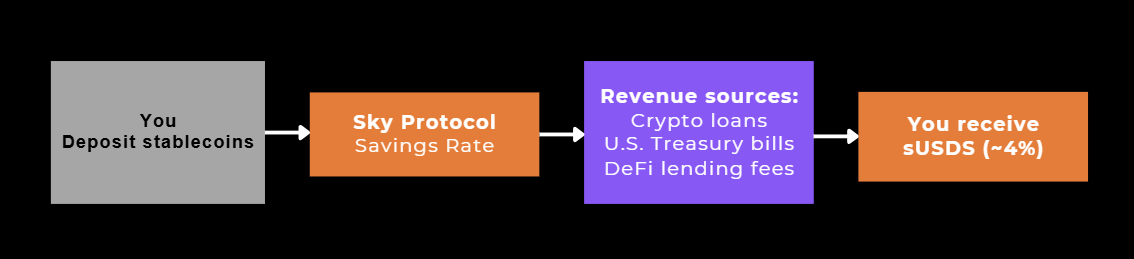

The idea: You deposit stablecoins, the protocol puts them to work (via lending, treasury bills, etc.), and passes the revenue back to you as yield. Simple, passive, no active management required.

How the yield flows: Your stablecoins → Protocol treasury → Deployed into overcollateralized loans + U.S. Treasury bills + DeFi lending → Revenue generated → Distributed back to depositors as yield

Sky Protocol (formerly MakerDAO) — sUSDS

Sky is the OG here. The protocol has been building in DeFi since 2015(formerly MakerDAO) and is one of the most battle-tested in the space. sUSDS is the world's largest yield-generating stablecoin with over $10 billion in supply, currently yielding around 4% APY.

How it works: You deposit USDS (or DAI, or USDC) into the Sky Savings Rate and receive sUSDS. The token's value increases over time as the protocol distributes yield. No lockups, so you can redeem instantly.

Where the yield comes from: The savings rate is funded by Sky's revenue, which includes fees from crypto-collateralized loans, investments into U.S. Treasury bills, and liquidity provisioning into SparkLend and the Spark Liquidity Layer. Spark Documentation This is real, organic revenue from one of DeFi's largest lending operations — not token emissions.

Key details:

Stablecoins accepted: USDS, DAI, USDC

Current yield: ~4–4.5% APY (set by governance, variable)

Available on: Ethereum, Base, Solana (via Wormhole), Arbitrum, OP Mainnet

Risk level: Low. Over-collateralized, audited smart contracts, 10+ years of MakerDAO history. Yield is variable and set by governance.

Who this is for: The "set it and forget it" crowd. If you want the closest thing to an on-chain savings account backed by real protocol revenue, this is it.

Check the transparency dashboard on fund allocations here: https://info.skyeco.com/collateral

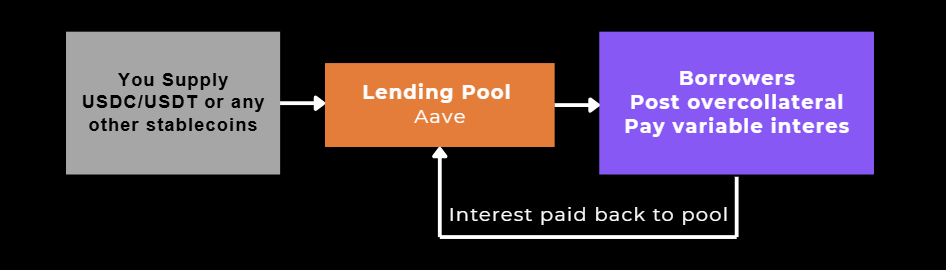

2. Lending Markets

The idea: You supply stablecoins to a lending pool. Borrowers pay interest to borrow your stablecoins (putting up collateral worth more than their loan). You earn a share of that interest.

How the yield flows: Your stablecoins → Lending pool (Aave, Morpho, Spark) → Borrowers pay interest on overcollateralized loans → Interest distributed to suppliers

A critical point most guides skip: not all lending is safe, and the risk depends entirely on what borrowers are posting as collateral. A pool backed by ETH and BTC as collateral carries very different risk from one backed by obscure tokens that could collapse in value. If collateral drops faster than liquidations can process, lenders can face losses. This is why the protocols we recommend here are Aave and Kamino, since they use DAO-curated markets, where the community votes on which collateral types are accepted and at what risk parameters. That governance layer is a meaningful safety filter.

Aave

Aave captures more than 80% of USDT and USDC deposits on Ethereum, translating to roughly $20 billion in stablecoin deposits. With cumulative loans exceeding $1 trillion originated and $40 billion in TVL, Aave is less a lending protocol and more the central bank of DeFi.

Current rates (as of late March 2026):

USDT supply APY: ~1.84%.

USDC supply APY: ~2.33%.

These are low right now — and that's the honest truth about lending yields. Aave rates are purely market-driven: when borrowing demand is high (bull market, leverage demand), supply rates spike. When demand is low (like now), rates compress. During peak periods in 2024–2025, USDC supply rates on Aave hit 8–12%.

Key point: Lending rates on Aave are not a fixed-income product. They're a real-time reflection of borrowing demand. Treat them as variables, and check rates before committing capital. Aave is best when you can catch periods of high utilization, which means that when the assets you are lending are borrowed by other people.

SparkLend

Part of the Sky ecosystem. SparkLend functions similarly to Aave but benefits from integration with Sky's liquidity layer, which actively deploys capital into the highest-yielding opportunities across protocols. The Spark Liquidity Layer operates across Ethereum, Base, Arbitrum, OP Mainnet, and Unichain, deploying liquidity into DeFi protocols like SparkLend, Aave, Morpho, and Curve, as well as RWA tokens backed by short-term U.S. Treasuries. Messari

Who this is for: Users who want a fully permissionless, transparent yield and understand that rates fluctuate. Best for capital that you're willing to move between protocols as conditions change.

Kamino (Solana)

Kamino is Solana's leading DeFi protocol. The largest stablecoin pool is the primary USDC market, currently holding more than $300 million USDC. Same mechanics as Aave — you supply stablecoins, borrowers pay interest. But Kamino also offers automated vault strategies (like USDC Prime) and Multiply (leveraged looping) for users who want more complex setups.

Current rates: The USDC lending yield varies dynamically with demand, spiking to over 20% during high-activity periods + incentives and falling to 2–3% during quieter times. Over the past 90 days, the average yield has stabilized around 5%. This is notably higher than Aave on Ethereum right now because Solana has more active leveraged trading demand.

Like Aave, Kamino uses governance-curated risk parameters to manage which collateral is accepted. That's the common thread between these two recommendations — the DAO as a risk filter, not just a yield source.

Incentivized Lending (Temporary Programs)

The idea: Sometimes, stablecoin issuers or protocols run promotional programs that temporarily boost lending yields through token rewards or direct subsidies. These aren't permanent — they come and go — but they can be very attractive while active.

How the yield flows: Your stablecoins → Deposit into incentivized pool/protocol → Earn base lending yield + bonus token rewards from issuer/protocol → Boosted total APY (temporary)

This is an important distinction. The base lending yield — from borrowers paying interest against the same DAO-curated collateral — doesn't change. The incentive is layered on top of it. So when PYUSD runs an incentive program on Spark, or RLUSD offers boosted rates on Aave, you're earning more from the same underlying lending activity, not taking on additional collateral risk to chase the higher number.

Examples of how this has worked:

PYUSD on Spark — PayPal ran a PYUSD Savings Vault offering 4.25% APY anchored to the Sky Savings Rate, with additional incentive programs to grow PYUSD deposits.

Maple's Syrup Seasons — The Syrup Seasons program has maintained an average total yield of 20.5% since launch, with Season 7 delivering an average total APY of 16.4%. These rewards are paid in $SYRUP tokens on top of the base lending yield. Seasons are time-limited.

Ripple's RLUSD on Aave — RLUSD currently offers 5.11% supply APY on, significantly above USDC/USDT rates — likely due to incentive programs driving early adoption.

How to spot these opportunities: Check DeFiLlama's yields dashboard, filter by stablecoins, and sort by APY. When you see a stablecoin with notably higher yields than comparable assets on the same protocol, there's usually an incentive program behind it. Key thing: always check whether the boosted rate is from incentives or organic demand, and know that incentive programs end.

Who this is for: Yield-optimizing farmers who actively monitor the market and are willing to rotate capital into temporary opportunities. Not a "set and forget" strategy.

3. Institutional Private Credit

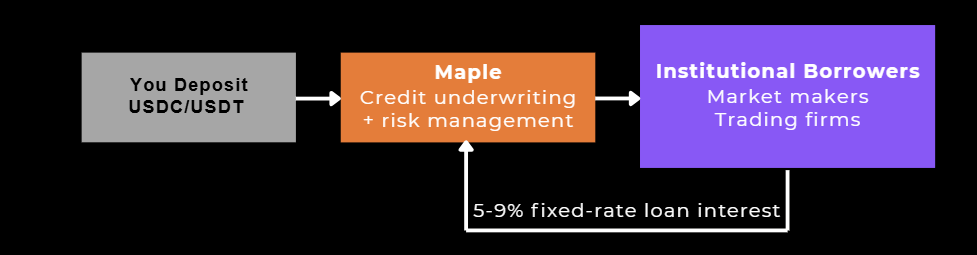

The idea: You deposit stablecoins into curated lending pools that fund vetted institutional borrowers (trading firms, market makers, crypto-native institutions). The protocol underwrites the credit risk.

How the yield flows: Your stablecoins → Maple's lending pools → Overcollateralized loans to vetted institutional borrowers (market makers, trading firms) → Borrowers pay 5–9% interest → Yield distributed to depositors

Maple Finance — syrupUSDC / syrupUSDT

Maple's deposits have surged past $4 billion, with syrupUSDC accounting for 63% of deposits. The protocol positions itself as the standard-bearer for on-chain institutional credit.

How it works: You deposit USDC or USDT and receive syrupUSDC or syrupUSDT — yield-bearing tokens that represent your share of Maple's lending pools. Yield comes from fixed-rate, overcollateralized loans extended to institutional borrowers through Maple's lending infrastructure.

Key details:

Stablecoins: USDC → syrupUSDC, USDT → syrupUSDT

Current yield: ~4–6% base APY (plus SYRUP token rewards during seasonal programs can push total yields significantly higher)

Available on: Ethereum, Solana, BNB Chain (expanding)

Maple issues short-duration loans at 5–9% to institutional borrowers, and passes the yield through to depositors

Risk level: Low-Medium. Overcollateralized and borrowers are vetted, but you're trusting Maple's credit underwriting. The protocol had historical credit events in 2022 (during the FTX/Alameda collapse) but has since restructured with stronger risk controls.

Composability bonus: syrupUSDC is integrated with Aave V3, Drift (as margin collateral), Kamino, and other protocols — meaning your yield-bearing stablecoin can be used as collateral elsewhere, stacking yields.

Who this is for: Users who want higher-than-lending-market yields with institutional-grade credit risk rather than smart-contract-only risk. Think of it as on-chain fixed income.

Maple Finance transparency dashboard: https://app.maple.finance/earn/details

4. RWA-Backed Yield: Tokenized Treasuries On-Chain

The idea: The stablecoin itself is backed by U.S. Treasury bills, and the yield flows directly to holders through a rising token price. No lending, no funding rates. Just government debt, brought on-chain.

How the yield flows: Your USDC → Protocol holds U.S. T-bills → Daily interest accrues → Reflected in rising token price → Redeem for more USDC than you put in

This is the most conservative yield in DeFi. Returns are lower than Maple or Ethena's bull-market peaks, but the underlying is U.S. government debt, not crypto-native risk.

Ondo Finance — USDY

Ondo is well known for tokenizing equities on-chain, but they also have a flagship stablecoin product for most DeFi users, USDY (US Dollar Yield Token), a tokenized note secured by short-term U.S. Treasuries and bank demand deposits, with assets held by a collateral agent to safeguard holders.

Where the yield comes from: Short-term U.S. Treasury bills and bank deposits. The token price rises daily as interest accrues — no staking, no claiming, no active management required.

USDY is issued from a separate, bankruptcy-remote legal entity, over-collateralized by a 3% first-loss position, and investors hold a first security interest in the underlying Treasuries with Ankura Trust acting as collateral agent. If Ondo Finance went bankrupt, USDY holders have legal claims over the underlying assets ahead of Ondo's creditors. Most stablecoins offer no such protection. Source of regulation: Ondo

Key details:

Current yield: ~3.5% APY (tracks short-term Fed rate, updated monthly)

Available on: Nine blockchains — Ethereum, Solana, Arbitrum, Sui, and more

Access: Non-U.S. individuals and institutions; KYC required; no minimum investment; note a 40–50 day initial lock-up before tokens are transferable on-chain

Risk level: Low. Yield tracks the Fed rate — when rates fall, yields compress. Smart contract risk applies as with any DeFi product.

5. Basis Trade / Delta-Neutral Yield

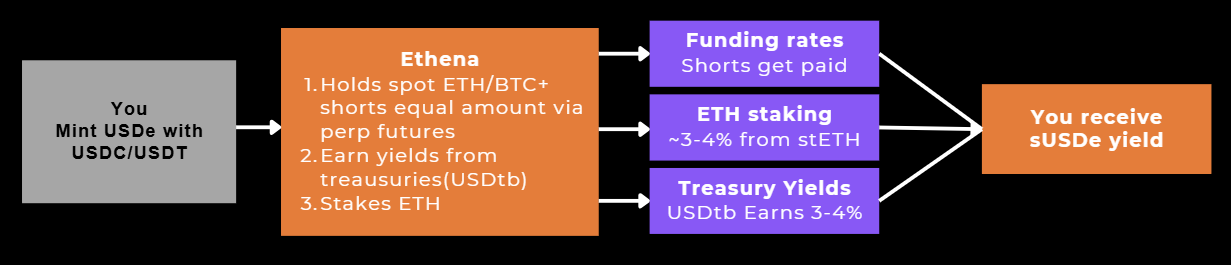

The idea: The protocol holds crypto collateral but shorts an equal amount via perpetual futures, creating a delta-neutral position. The yield comes from funding rates paid by leveraged longs to shorts.

How the yield flows: Your stablecoins → Mint USDe (backed by ETH/BTC + short futures) → Funding rates from perps markets + ETH staking rewards → Revenue distributed to sUSDe holders

Ethena — USDe / sUSDe

Ethena launched USDe in February 2024 as a dollar-pegged stablecoin that earns yield without bank reserves, backing itself entirely through crypto derivatives. It has become the third-largest stablecoin in existence.

How it works: You buy USDe and stake it into sUSDe. The protocol holds spot ETH/BTC and simultaneously shorts the same amount in perpetual futures. This delta-neutral position earns funding rates (perpetual shorts typically get paid when the market is bullish) plus ETH staking rewards from the collateral.

Where the yield comes from: Ethena generates yield from three sources: perpetual futures funding rates (the primary source), ETH staking yield from consensus and execution layers, and interest on liquid stablecoins like USDtb (backed by BlackRock's BUIDL fund), USDC, and USDT.

Critically, during periods where funding rates yield less than U.S. Treasuries — typically during market downturns — Ethena allocates a higher proportion of USDe backing to liquid stablecoins.So the protocol dynamically shifts between crypto-heavy and stablecoin/treasury-heavy backing depending on market conditions. The reserve fund (currently held in USDtb, which is backed by BlackRock's BUIDL tokenized treasury fund) acts as a buffer for negative funding periods.

Key details:

Stablecoin: USDe → stake for sUSDe

Current yield: ~3.5–4% APY (as of March 2026 — down from peaks of 15–27% during bull markets)

Available on: Ethereum + 24 chains

Risk level: Medium. This is higher risk than Sky. In 2025, sUSDe yields ranged from approximately 4–15%, reflecting the variable nature of funding rates. StablecoinInsider During bear markets, funding rates can go negative, which compresses or eliminates yield. There's also counterparty risk from the centralized exchanges used for hedging, and a 7-day unstaking cooldown.

The key thing to understand: Ethena's yield is cyclical. In bull markets, when everyone is leveraged long, funding rates are high and sUSDe yields spike. In bear/sideways markets, yields compress. Right now we're in a compressed period. This isn't broken, it's how the mechanism works.

Who this is for: Traders who understand funding rate dynamics and want higher yield potential with the understanding that returns are variable and tied to market conditions.

Ethena transparency dashboard: app.ethena.fi/dashboards/transparency

General Risk Warnings

Smart contract risk applies to everything here. Even audited protocols can have bugs. Spread across multiple protocols rather than concentrating everything in one.

Yield is never guaranteed. Every rate in this guide is variable. Sky's savings rate is set by governance and can change. Ethena's yield depends on market conditions. Aave rates fluctuate hourly. Maple's rates depend on credit demand.

Understand what backs your stablecoin. USDC and USDT are fiat-backed. USDS/DAI are crypto-overcollateralized. USDe is delta-neutral synthetic. Each has a different risk profile, even before you layer on yield.

Regulatory risk is real. The GENIUS Act (U.S.) and MiCA (EU) are defining new rules for stablecoins. Some products may need to adapt or restrict access depending on your jurisdiction.

If you can't explain where the yield comes from, you are the yield. This remains the single most important rule in DeFi.

So, Where Do I have to start?

If you're new to stablecoin yields, start with Sky's sUSDS via Spark (spark.fi). It's the largest, most battle-tested option with real organic yield and no lockups. Deposit USDC, USDS, or DAI, receive a yield-bearing token, and your balance grows automatically.

From there, you can explore Maple for higher yields with institutional credit exposure, or watch for incentivized lending programs that temporarily boost returns on specific stablecoins.

The stablecoin yield landscape is maturing fast. Every idle dollar in DeFi is now a dollar losing money — with 4–5% yields embedded directly into stablecoin tokens, the sector is on track to surpass $50 billion by end of 2026. Blockeden

Your stablecoins should be working. Now you know where to put them.